SCHEME OF WORK

WEEK TOPIC

1. Revision of First Term’s work

2. Bank service: commercial bank – services provided by commercial banks, Ethical issue in banking

3. Insurance: definition of insurance, insurance services, types of insurance policy – vehicle, fire, burglary, marine, Life insurance, pension, health, etc and benefits of insurance

4. Book keeping – Ledger Entries: ledger, meaning of ledger, items on a ledger – date, particulars, folio, Discount – amount, how to record cash receive payments = discount received, discount allowed and contra entries

5. Book keeping – petty cash book: meaning of petty cash book, preparation of petty cash book, imp rest system – petty cash, refinement and reimbursement.

6. Cash Book; Meaning of cash book, types of cash book – single column cash book, two/double column cash book, items on a column cash – cash column, bank column and discount column, preparation of cash book – cash column, bank column and discount column, preparation of cash book.

7. Pitman shorthand(vowel placement): Vowels: Placement(first second and third), Types (eeou), word drills.

8. Pitman shorthand(Third group of consonants and vowel): Consonants and Vowels – Third group of consonants ( k, g m, n, ng, I , w, y), first place Vowels(ah, oo, aw), Third place( e, I, oo, oo)

9. Pitman shorthand (consonant R & H): Consonant Vowels – The fourth(last group of consonants (R & H), Forems or R & H – Upward, Downward, Diphthongs and triphone – meaning , shorthand outlines and signs.

10. Revision

2ND TERM

WEEK 1

Bank and Their Services

Preview

1. Bank service: commercial banks

2. Functions/Services provided by commercial banks,

3. Ethical issues in banking

Full Content

Banks are public limited liability companies that are in the business of providing financial services to consumers and businesses. They receive, transfer, pay, exchange, lend, invest and safeguard money for people or companies.

COMMERCIAL BANKS

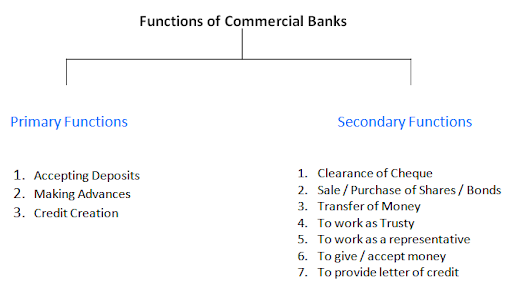

A commercial bank is a financial institution that renders financial services to customers. It performs a number of functions which are listed below:

FUNCTIONS OF COMMERCIAL BANKS/SERVICES PROVIDED BY

1. Accepting deposits from depositors/customers

2. Keeping money and valuables in safety for customers

3. Assisting customers with loan and overdraft to start or expand their business

4. Giving financial/investment advice to customers

5. Trading in foreign currency and giving traveler’s cheque to customers travelling abroad.

6. Assisting customers to transfer money from one country to another

7. Acting as a trustee or guarantor on behalf of their customers.

Let’s take a closer look into each of the functions.

FUNCTIONS/SERVICES OF COMMERCIAL BANKS

1. Acceptance of Deposit: By accepting deposits from borrowers and then lending the money to borrowers, banks encourage the flow of money to productive use and investment. This in turn allows the economy to grow.

2. Keeping Valuables in Safety for Customers: Commercial banks help in safe-keeping valuables such as jewelries, company’s share certificates, etc and thereby prevent such from being stolen or damaged.

3. Assisting Customers with Loans: This effort provide ready fund to those who want to engage in business but lack the fund to go into such businesses.

4. Giving Financial Advice to Customers: This helps prevent taking risk that could affect customers financially.

ETHICAL ISSUES IN BANKING

1. Banks should keep all financial matters of individuals confidential.

2. Bank officials must keep customer’s account accurate.

3. Officials of bank must avoid stealing from the bank.

4. Bank clerks must not steal from customers.

5. Banks must follow government regulation.

6. Bank should not give false report to the government.

7. There should be no cover up of customers’ financial crime.

8. All documents related to criminal activities must be made available to the appropriate government agencies when demanded.

EVALUATION

Objectives:

1. Which of the following is not among banking services

a. Loans b. Traveller’s Cheque c. Banker’s draft

2. Which of the following is not an ethical issue in the banking sector?

a. Confidentiality b. Integrity c. Non-transparency

Theory:

3. Define a commercial bank.

4. When banks allow customers to draw more money than he has in his bank account, this is called_____________

MAIN TOPIC: BANK SERVICES

SPECIFIC TOPIC: Commercial banks

REFERENCE BOOKS:

Macmillan JSS2 Business Studies by Awoyokun A.A et al .Pages 30-36

WABP JSS Business Studies 2 by Egbe T. Ehiametalor. Pages 58-61

PERFORMANCE OBJECTIVES: At the end of the lesson, students should be able to:

define a commercial bank

mention examples of commercial banks

CONTENTS:

Banks are places where money is kept until the owner requires it.

Commercial banks are places for keeping money and other valuables such as jewelries and important documents.

The most important function of the commercial bank is the safe keeping of money until the owner needs it.

Examples of commercial banks are: Zenith bank, Access bank, GTB First bank etc.

EVALUATION:

What is commercial bank

mention five examples of commercial banks around you.

HOME-WORK: mention five services provided by commercial banks

LESSON 53

MAIN TOPIC: BANK SERVICES

SPECIFIC TOPIC: Commercial banks

REFERENCE BOOKS:

Macmillan JSS2 Business Studies by Awoyokun A.A et al .Pages 30-36

WABP JSS Business Studies 2 by Egbe T. Ehiametalor. Pages 58-61

PERFORMANCE OBJECTIVES: At the end of the lesson, students should be able to:

define a commercial bank

mention examples of commercial banks

CONTENTS:

Banks are places where money is kept until the owner requires it.

Commercial banks are places for keeping money and other valuables such as jewelries and important documents.

The most important function of the commercial bank is the safe keeping of money until the owner needs it.

Examples of commercial banks are: Zenith bank, Access bank, GTB First bank etc.

EVALUATION:

What is commercial bank

mention five examples of commercial banks around you.

HOME-WORK: mention five services provided by commercial banks

further studies

http://education-portal.com/academy/les ... tml#lesson

http://www.preservearticles.com/2012033 ... banks.html

https://www.classle.net/book/functions-commercial-banks#

practice test

http://wizznotes.com/pob/business-finance/quiz

http://www.financialquiz.net/financialquiz.php

http://homes.chass.utoronto.ca/~reak/ec ... iz12v3.htm mention examples of commercial banks

Preview

1. Bank service: commercial banks

2. Functions/Services provided by commercial banks,

3. Ethical issues in banking

Full Content

Banks are public limited liability companies that are in the business of providing financial services to consumers and businesses. They receive, transfer, pay, exchange, lend, invest and safeguard money for people or companies.

COMMERCIAL BANKS

A commercial bank is a financial institution that renders financial services to customers. It performs a number of functions which are listed below:

FUNCTIONS OF COMMERCIAL BANKS/SERVICES PROVIDED BY

1. Accepting deposits from depositors/customers

2. Keeping money and valuables in safety for customers

3. Assisting customers with loan and overdraft to start or expand their business

4. Giving financial/investment advice to customers

5. Trading in foreign currency and giving traveler’s cheque to customers travelling abroad.

6. Assisting customers to transfer money from one country to another

7. Acting as a trustee or guarantor on behalf of their customers.

Let’s take a closer look into each of the functions.

FUNCTIONS/SERVICES OF COMMERCIAL BANKS

1. Acceptance of Deposit: By accepting deposits from borrowers and then lending the money to borrowers, banks encourage the flow of money to productive use and investment. This in turn allows the economy to grow.

2. Keeping Valuables in Safety for Customers: Commercial banks help in safe-keeping valuables such as jewelries, company’s share certificates, etc and thereby prevent such from being stolen or damaged.

3. Assisting Customers with Loans: This effort provide ready fund to those who want to engage in business but lack the fund to go into such businesses.

4. Giving Financial Advice to Customers: This helps prevent taking risk that could affect customers financially.

ETHICAL ISSUES IN BANKING

1. Banks should keep all financial matters of individuals confidential.

2. Bank officials must keep customer’s account accurate.

3. Officials of bank must avoid stealing from the bank.

4. Bank clerks must not steal from customers.

5. Banks must follow government regulation.

6. Bank should not give false report to the government.

7. There should be no cover up of customers’ financial crime.

8. All documents related to criminal activities must be made available to the appropriate government agencies when demanded.

EVALUATION

Objectives:

1. Which of the following is not among banking services

a. Loans b. Traveller’s Cheque c. Banker’s draft

2. Which of the following is not an ethical issue in the banking sector?

a. Confidentiality b. Integrity c. Non-transparency

Theory:

3. Define a commercial bank.

4. When banks allow customers to draw more money than he has in his bank account, this is called_____________

MAIN TOPIC: BANK SERVICES

SPECIFIC TOPIC: Commercial banks

REFERENCE BOOKS:

Macmillan JSS2 Business Studies by Awoyokun A.A et al .Pages 30-36

WABP JSS Business Studies 2 by Egbe T. Ehiametalor. Pages 58-61

PERFORMANCE OBJECTIVES: At the end of the lesson, students should be able to:

define a commercial bank

mention examples of commercial banks

CONTENTS:

Banks are places where money is kept until the owner requires it.

Commercial banks are places for keeping money and other valuables such as jewelries and important documents.

The most important function of the commercial bank is the safe keeping of money until the owner needs it.

Examples of commercial banks are: Zenith bank, Access bank, GTB First bank etc.

EVALUATION:

What is commercial bank

mention five examples of commercial banks around you.

HOME-WORK: mention five services provided by commercial banks

LESSON 53

MAIN TOPIC: BANK SERVICES

SPECIFIC TOPIC: Commercial banks

REFERENCE BOOKS:

Macmillan JSS2 Business Studies by Awoyokun A.A et al .Pages 30-36

WABP JSS Business Studies 2 by Egbe T. Ehiametalor. Pages 58-61

PERFORMANCE OBJECTIVES: At the end of the lesson, students should be able to:

define a commercial bank

mention examples of commercial banks

CONTENTS:

Banks are places where money is kept until the owner requires it.

Commercial banks are places for keeping money and other valuables such as jewelries and important documents.

The most important function of the commercial bank is the safe keeping of money until the owner needs it.

Examples of commercial banks are: Zenith bank, Access bank, GTB First bank etc.

EVALUATION:

What is commercial bank

mention five examples of commercial banks around you.

HOME-WORK: mention five services provided by commercial banks

further studies

http://education-portal.com/academy/les ... tml#lesson

http://www.preservearticles.com/2012033 ... banks.html

https://www.classle.net/book/functions-commercial-banks#

practice test

http://wizznotes.com/pob/business-finance/quiz

http://www.financialquiz.net/financialquiz.php

http://homes.chass.utoronto.ca/~reak/ec ... iz12v3.htm mention examples of commercial banks

WEEK 2

INSURANCE

Preview

1. Insurance: definition of insurance.

2. Insurance services.

3. Types of insurance policy – vehicle, fire, burglary, marine, Life insurance, pension, health, etc

4. Benefits of insurance

Full Content

Meaning of insurance: insurance is the protection against the loss of property and life. With regard to property, insurance covers practically everything an individual or business owns (building, vehicles and even clothes). Insurance can be taken out on practically anything for which risk is associated.

Insurance is usually undertaken when a person enters into an agreement with an insurance company by paying an amount of money called the Premium. The company is known as the Insurer. The person who pays the premium is the insured.

SERVICES PROVIDED BY INSURANCE COMPANIES

1. It provides compensation for losses incurred by individuals and businesses

2. It minimizes losses and risks by spreading it through the creation of a common fund to which many contribute in order to make good the losses of a few.

3. It aids business survival and help them to quickly recover economically from natural or man-made disaster.

4. To help families whose breadwinners may die accidentally while at work

5. Provide sources of fund in case of health break down.

6. Provide continuous funds for those who have retired.

TYPES OF INSURANCE

1. Vehicle insurance: This form of insurance can be taken by any person or business that owns a car. Once an individual has taken out such an insurance, that person is covered against a specific loss.

FORMS OF VEHICLE INSURANCE COVERAGE

• Third party insurance: This policy allows a driver whose car is hit by another car to file a claim against other who is wrong and who holds this type of policy. In other words, the insurance company insures the person which the policy holder may accidentally hit. It provides protection against liability caused by a car accident.

• Comprehensive Insurance: This policy covers the loss incurred by the individual who took out the policy and the person he accidentally hit. The policy holder can also recover a certain percentage, as high as 80% of the cost of the car, if it is stolen, washed away by flood or damaged by a fallen tree.

2. Fire insurance: is a coverage against fire hazards which may consume business premises or personal property. In recent years, there have been numerous fire hazards in public buildings. The Republic building in Lagos state, the Cocoa House in Ibadan, the Pay Office in Abuja and NNPC office complex in Lagos and some examples of high rise buildings destroyed by fire in Nigeria. The losses associated with this buildings would have been enormous but for the fact that the owner of this building had insured them against fire hazards. At the occurrence of such fires, the insurance company would pay a sum agreed at the time of insurance.

3. Burglary or Theft insurance: This type of policy covers loss of, or damage to property in the event of burglary or theft. Items that are insured under this class of insurance stock, plant and machinery, household effects, office equipment, etc

4. Marine/Sea Insurance: This is one of the oldest types of insurance. Cover provided by a marine insurance policy is limited to dangers on water, that is, it covers loss of, or damage to ships, and the cargo carried by them.

5. Life Assurance: Life assurance serves a dual purpose. It is a means of reducing the financial burden of a family which the bread winner may bring. It is also a method of saving.

Life assurance is always for a specific period of time during which the assured continues to pay his or her premiums. The payment of such premium may be yearly, quarterly or monthly.

In the event of the assured’s death, the insurance company pays out the sum assured by the policy.

Types of Life Assurance

• Whole life assurance: This policy ensures the payment of the amount of money due at the death of the assured.

• Endowment assurance: This policy is taken up for a specific period, e.g. twenty years.

BENEFITS OF INSURANCE

• Protects capital assets against such risks as fire, theft, accidents.

• Enables the policy holder to form the habit of saving regularly

• Helps the assured to obtain loan for some future business or other projects. For example, in certain circumstances, life assurance can be used as a security for loan.

• Provides cash (an income benefit) for the dependants of the policy holder in the event of death.

• Ensures that worries and embarrassment that might make an individual unhappy and removed, since he is certain that any loss or damaged suffered by him will be made good by the insurance company.

EVALUATION

Objectives:

1. Which of the following is the purpose of insurance? (a) to make profit (b) to make good the loss suffered (c)to collect premium (d) to avoid loss

2. One of the insurance policy is not for motor vehicle (a) third party(b) marine(c) comprehensive (d) theft

3. All the risk stated below are not insurable except (a)storm(b) earthquake(c) gambling (d) thefts

4. What is the sum of money paid by the insured to the insurance company called? (a) discount (b) commission (c) premium (d) dividend

Theory:

1. What is insurance?

2. Why is insurance important to the businessman or individual taking out a policy?

3. What are the benefits of insurance?

MAIN TOPIC: INSURANCE

SPECIFIC TOPIC: Types of Insurance

REFERENCE BOOKS:

Macmillan JSS1 Business Studies by Awoyokun A.A et al .Pages 37-45

WABP JSS Business Studies 1by Egbe T. Ehiametalor. Pages 62-66

PERFORMANCE OBJECTIVES: At the end of the lesson, students should be able to:

mention types of Insurance

explain the different types of Insurance

CONTENTS:

TYPES OF INSURANCE

Vehicle Insurance

Fire Insurance

Burglary Insurance

Marine Insurance

Pension Insurance Scheme

Health Insurance

Agricultural Insurance

Life Assurance

FIRE INSURANCE: This is coverage against fire accidents which may consume business premises or personal property.

BURGLARY OR THEFT INSURANCE: Business premises may be burgled especially during the night. This type of insurance will enable the business man to recover the value of the items burgled.

MARINE INSURANCE: This is a kind of insurance against risks involved when goods are carried by sea. The policy covers both the ship carrying the goods and the goods themselves.

EVALUATION:

mention five types of Insurance

explain three out of the types of Insurance mentioned

HOME-WORK: explain Life Assurance

further studies

http://www.gruenden.ch/en/founding-proc ... -security/

http://typesofinsurance.org/

http://www.insuranceinfo.com.my/choose_ ... efLangID=1&

LESSON 49

MAIN TOPIC: INSURANCE

SPECIFIC TOPIC: Advantages and disadvantages of insurance

REFERENCE BOOKS:

Macmillan JSS1 Business Studies by Awoyokun A.A et al .Pages 25-29

WABP JSS Business Studies 1by Egbe T. Ehiametalor. Page 50-57

PERFORMANCE OBJECTIVES: At the end of the lesson, students should be able to:

mention advantages of insurance

mention the disadvantages of insurance

CONTENTS:

ADVANTAGES

It eases or reduces the burden of loss on the individual or business taking out the policy

Risks of ownership are minimized

Although life cannot be restored by any insurance policy, the surviving members of a family can be adequately compensated to minimize hardship.

DISADVANTAGES

Some insurance companies usually dodge payment of compensation to the insured when it is necessary to do so.

EVALUATION: Mention two advantages and two disadvantages of insurance

HOME-WORK: What is banking?

further studies

https://www.360financialliteracy.org/To ... -insurance

http://www.insuranceresearchers.com/adv ... insurance/

http://www.prokerala.com/banking/articl ... option.php

practice test

http://www.quibblo.com/quiz/a1aulgo/Gen ... rance-Exam

http://www.insuranceinfo.com.my/help_an ... efLangID=1&

http://www.proprofs.com/quiz-school/sto ... ise-exam-1

http://www.insureuonline.org/quiz_under30.htm

http://netlearnnow.com/aie-folder/free_ ... quiz1.html

Preview

1. Insurance: definition of insurance.

2. Insurance services.

3. Types of insurance policy – vehicle, fire, burglary, marine, Life insurance, pension, health, etc

4. Benefits of insurance

Full Content

Meaning of insurance: insurance is the protection against the loss of property and life. With regard to property, insurance covers practically everything an individual or business owns (building, vehicles and even clothes). Insurance can be taken out on practically anything for which risk is associated.

Insurance is usually undertaken when a person enters into an agreement with an insurance company by paying an amount of money called the Premium. The company is known as the Insurer. The person who pays the premium is the insured.

SERVICES PROVIDED BY INSURANCE COMPANIES

1. It provides compensation for losses incurred by individuals and businesses

2. It minimizes losses and risks by spreading it through the creation of a common fund to which many contribute in order to make good the losses of a few.

3. It aids business survival and help them to quickly recover economically from natural or man-made disaster.

4. To help families whose breadwinners may die accidentally while at work

5. Provide sources of fund in case of health break down.

6. Provide continuous funds for those who have retired.

TYPES OF INSURANCE

1. Vehicle insurance: This form of insurance can be taken by any person or business that owns a car. Once an individual has taken out such an insurance, that person is covered against a specific loss.

FORMS OF VEHICLE INSURANCE COVERAGE

• Third party insurance: This policy allows a driver whose car is hit by another car to file a claim against other who is wrong and who holds this type of policy. In other words, the insurance company insures the person which the policy holder may accidentally hit. It provides protection against liability caused by a car accident.

• Comprehensive Insurance: This policy covers the loss incurred by the individual who took out the policy and the person he accidentally hit. The policy holder can also recover a certain percentage, as high as 80% of the cost of the car, if it is stolen, washed away by flood or damaged by a fallen tree.

2. Fire insurance: is a coverage against fire hazards which may consume business premises or personal property. In recent years, there have been numerous fire hazards in public buildings. The Republic building in Lagos state, the Cocoa House in Ibadan, the Pay Office in Abuja and NNPC office complex in Lagos and some examples of high rise buildings destroyed by fire in Nigeria. The losses associated with this buildings would have been enormous but for the fact that the owner of this building had insured them against fire hazards. At the occurrence of such fires, the insurance company would pay a sum agreed at the time of insurance.

3. Burglary or Theft insurance: This type of policy covers loss of, or damage to property in the event of burglary or theft. Items that are insured under this class of insurance stock, plant and machinery, household effects, office equipment, etc

4. Marine/Sea Insurance: This is one of the oldest types of insurance. Cover provided by a marine insurance policy is limited to dangers on water, that is, it covers loss of, or damage to ships, and the cargo carried by them.

5. Life Assurance: Life assurance serves a dual purpose. It is a means of reducing the financial burden of a family which the bread winner may bring. It is also a method of saving.

Life assurance is always for a specific period of time during which the assured continues to pay his or her premiums. The payment of such premium may be yearly, quarterly or monthly.

In the event of the assured’s death, the insurance company pays out the sum assured by the policy.

Types of Life Assurance

• Whole life assurance: This policy ensures the payment of the amount of money due at the death of the assured.

• Endowment assurance: This policy is taken up for a specific period, e.g. twenty years.

BENEFITS OF INSURANCE

• Protects capital assets against such risks as fire, theft, accidents.

• Enables the policy holder to form the habit of saving regularly

• Helps the assured to obtain loan for some future business or other projects. For example, in certain circumstances, life assurance can be used as a security for loan.

• Provides cash (an income benefit) for the dependants of the policy holder in the event of death.

• Ensures that worries and embarrassment that might make an individual unhappy and removed, since he is certain that any loss or damaged suffered by him will be made good by the insurance company.

EVALUATION

Objectives:

1. Which of the following is the purpose of insurance? (a) to make profit (b) to make good the loss suffered (c)to collect premium (d) to avoid loss

2. One of the insurance policy is not for motor vehicle (a) third party(b) marine(c) comprehensive (d) theft

3. All the risk stated below are not insurable except (a)storm(b) earthquake(c) gambling (d) thefts

4. What is the sum of money paid by the insured to the insurance company called? (a) discount (b) commission (c) premium (d) dividend

Theory:

1. What is insurance?

2. Why is insurance important to the businessman or individual taking out a policy?

3. What are the benefits of insurance?

MAIN TOPIC: INSURANCE

SPECIFIC TOPIC: Types of Insurance

REFERENCE BOOKS:

Macmillan JSS1 Business Studies by Awoyokun A.A et al .Pages 37-45

WABP JSS Business Studies 1by Egbe T. Ehiametalor. Pages 62-66

PERFORMANCE OBJECTIVES: At the end of the lesson, students should be able to:

mention types of Insurance

explain the different types of Insurance

CONTENTS:

TYPES OF INSURANCE

Vehicle Insurance

Fire Insurance

Burglary Insurance

Marine Insurance

Pension Insurance Scheme

Health Insurance

Agricultural Insurance

Life Assurance

FIRE INSURANCE: This is coverage against fire accidents which may consume business premises or personal property.

BURGLARY OR THEFT INSURANCE: Business premises may be burgled especially during the night. This type of insurance will enable the business man to recover the value of the items burgled.

MARINE INSURANCE: This is a kind of insurance against risks involved when goods are carried by sea. The policy covers both the ship carrying the goods and the goods themselves.

EVALUATION:

mention five types of Insurance

explain three out of the types of Insurance mentioned

HOME-WORK: explain Life Assurance

further studies

http://www.gruenden.ch/en/founding-proc ... -security/

http://typesofinsurance.org/

http://www.insuranceinfo.com.my/choose_ ... efLangID=1&

LESSON 49

MAIN TOPIC: INSURANCE

SPECIFIC TOPIC: Advantages and disadvantages of insurance

REFERENCE BOOKS:

Macmillan JSS1 Business Studies by Awoyokun A.A et al .Pages 25-29

WABP JSS Business Studies 1by Egbe T. Ehiametalor. Page 50-57

PERFORMANCE OBJECTIVES: At the end of the lesson, students should be able to:

mention advantages of insurance

mention the disadvantages of insurance

CONTENTS:

ADVANTAGES

It eases or reduces the burden of loss on the individual or business taking out the policy

Risks of ownership are minimized

Although life cannot be restored by any insurance policy, the surviving members of a family can be adequately compensated to minimize hardship.

DISADVANTAGES

Some insurance companies usually dodge payment of compensation to the insured when it is necessary to do so.

EVALUATION: Mention two advantages and two disadvantages of insurance

HOME-WORK: What is banking?

further studies

https://www.360financialliteracy.org/To ... -insurance

http://www.insuranceresearchers.com/adv ... insurance/

http://www.prokerala.com/banking/articl ... option.php

practice test

http://www.quibblo.com/quiz/a1aulgo/Gen ... rance-Exam

http://www.insuranceinfo.com.my/help_an ... efLangID=1&

http://www.proprofs.com/quiz-school/sto ... ise-exam-1

http://www.insureuonline.org/quiz_under30.htm

http://netlearnnow.com/aie-folder/free_ ... quiz1.html

WEEK 3

Topic: Book Keeping - Ledger Entries

PREVIEW

1. Book keeping – Ledger Entries: ledger, meaning of ledger,

2. Items on a ledger – date, particulars, folio, Discount – amount,

3. How to record cash received/payments: discount received, discount allowed and contra entries

Full Content

Meaning of Ledger:

A ledger is the principal book of account where all accounting entries are recorded. It usually has numbered pages to enable it to be easily identified from other book of account. Each page is called a Folio, and the number in it is called Folio number. A Ledge is drawn as follows:

ITEMS ON A LEDGER/LEDGER ENTRIES

DEBIT (DR) CREDIT(CR)

DATE PARTICULARS FOLIO AMOUNT DATE PARTICULARS FOLIO AMOUNT

N K N K

Entries on the left side are DEBIT ENTRIES Entries on the right side are CREDIT ENTRIES

1. Date: this column is for recording the day, mount and year the transaction took place

2. Particulars: this column explains the type of transaction that took place, e. g sales, purchase and name of individual that is involved in the transaction

3. Folio: this column is used in entering the page number of the journal from which from which the posting to the ledger account is made

4. Discount: this column is for entering the discount received for proper reconciliation when cost is being calculated.

5. Amount: this column is used to record the actual monetary value in Naira and Kobo.

HOW TO RECORD CASH RECEIVED/PAYMENT

EXAMPLE: If Mr. Hassan made the following transactions, they will be posted in a three – column cash book:

March 1. Cash at hand 200

Cash in bank 2,000

1. Withdrawal of office cash 300

2 Customer R. Adelai settle his account of

N200 by cash and was allowed 5% discount

4 Paid wages by cheque 700

5 Receive cheque from R.Winla 1,160

5 Allowed him discount 0

5 Purchase of goods less 5% discount

(Discount received) by cash 400

6 Paid T. Chike by cheque 280

Discount received 20

6 Bought packaging materials for cash 20

7 Cash sales 3,000

7 Paid into bank 2,800

What was the balance brought down on 7th Mar,2005?

Mr. Hassan’s Three Column Cash Book for March 2005

Date Particulars Folio Disct. Allwd Cash Bank Date Particulars Folio Disct. Received Cash Bank

Mar 1

Mar 2

Mar 2

Mar 5

Mar 7

Mar 7

Oct. 1 Balance

Bank

R. Adelai

R. Winla

Sales

Cash

Balance b/d

cc

b/d

10

40

200

300

190

3000

2,000

1160

2,800 Mar 2

Mar 4

Mar 5

Mar 6

Mar 6

Mar 7

Mar 7 Office Cash

Wages

Purchases

T. Chike

Packing mat.

Bank

Balance

cc

20

20

380

20

2,800

490 300

700

280

4,680

50 3,690 5,960 40 4,500 8,000

490 4,680

From Mr. Hassan’s Cash Book, the following ledgers can be drawn:

Dr Office A/c Cr

Date Particulars Amount N Date Particulars Amount

Mar 2

Bank 300

Dr Bank A/c Cr

Date Particulars Amount N Date Particulars Amount

Mar 2 Bank

300

Dr R. Adelai A/c Cr

Date Particulars Amount N Date Particulars Amount

Apr 1 Balance c/d 200 Mar 2

Mar 2 Cash

Discount 190

10

Dr Wages A/c Cr

Date Particulars Amount N Date Particulars Amount

Mar 4

Bank 700

Dr R. Winla A/c Cr

Date Particulars Amount N Date Particulars Amount

Apr 1

Balance b/d 1,200 Mar 5

Mar 5 Bank

Discount 1,160

40

1,200

Dr Purchase A/c Cr

Date Particulars Amount N Date Particulars Amount

Mar 5

Mar 5

Cash

Discount 380

20 Apr 1 Balance c/d 400

400

Dr T. Chike A/c Cr

Date Particulars Amount N Date Particulars Amount

Mar 6

Mar 6

Bank

Discount 280

20 Apr 1 Balance c/d 300

300

Dr Packing Materials A/c Cr

Date Particulars Amount N Date Particulars Amount N

Mar 6

Cash 20

Dr Sales A/c Cr

Date Particulars Amount N Date Particulars Amount N

Mar 7 Cash 800

Dr Discount Received A/c Cr

Date Particulars Amount N Date Particulars Amount

Mar 5

Mar 6

Purchases

T. Chike 20

20 Apr 1 Balance c/d 40

40

Dr Discount Allowed A/c Cr

Date Particulars Amount N Date Particulars Amount

Mar 2

Mar 5 R. Adelai

R. Winla 10

40

Dr Cash Account Cr

Date Particulars Amount N Date Particulars Amount N

Mar 7 Cash 2,800

Further Explanations

1. Discount Received: This is the cash rebate given to the seller by his suppliers of goods. It is recorded on the credit side of the cash book and on the debit side of the ledger

2. Discount Allowed: This is the cash rebate given to the buyers of goods by the seller. It is usually recorded on the debit side of the cash book and on the credit side of the ledger.

3. Contra Entries: the word contra is a Latin word meaning opposite. In some cases in business, there may be excess cash in hand which needs to be paid into the bank for official use. These are known as contra entries because both sides of the cash book will have entries concerning each transaction. Contra entries are denoted by “c” or “cc” in the folio columns and on the ledger. A bank that is credited in the cash book will be debited, while cash debited on the cash book will be credited.

EVALUATION

Objectives:

1. ___________ is not a column in the ledger. (a) Date B. Folio C. Cash

2. _________ is a column for entering page numbers. A. Particulars B. Folio C. Discount

3. The debit side of the ledger is at the _______ A. left-hand side B. right-hand side C. centre side

4. The column used for recording the actual monetary value is called ______ A. folio B. discount C. Amount

Theory:

1. Define Ledger

2. List four items posted on the debit side of a ledger

Record the following in the appropriate ledger account of Tochukwu Nwufo:

2. a. Folio 28

Jan 1 he owed the business N2000

Jan 10 he was goods worth N3,500

Jan 15 he paid N4,000 cash to the business

Jan 22, receive a debt note of N550

Jan 25 receive a credit note of N150

WEEK 5

BOOK KEEPING: Petty Cash Book

Preview

1. Book keeping – petty cash book: meaning of petty cash book,

2. preparation of petty cash book,

3. Imprest system – petty cash, refinement and reimbursement.

Full Content

PETTY CASH BOOK

This is used to record small expenses such as postage stamps, envelops, transport fares, newspapers, stationery and other small items needed in the office. The word ‘petty’ means small or unimportant. We cannot pay for them with cheques because they are too small. It is also a book of original entry and also a ledger account for petty cash. The cost of each of the small items is recorded in the petty cash book instead of the ledger. The total expenses are transferred to the ledger as a petty cash account.

Columns In a Petty Cash Book

DEBIT SIDE

1. Amount

2. Date

3. Particulars of expenses

4. Voucher number

5. Total amount

CREDIT SIDE

On the credit side we have the analysis of expenses of a ledger account. This has different columns for different expenses e. g stationery, postage, transport, etc.

Recording of Receipts and Payments in Petty Cash Book

1. The credit entry is made in the cash book

2. The debt entry is made in the petty cash book

3. The entries on the credit side of the petty cash book are first made in the total column and then, extended into the relevant expenses column,

4. The expenses columns have various headings for different expenses,

5. The last column of the petty cash book is known as a ledger account.

Preparation of a Petty Cash Book

Example

Record the following in the relevant columns of the petty cash book of Chillington, a sole proprietor.

Jan 1. Petty cashier received an Imprest amount of N2000

2 Paid for bus fare N200

4 Paid for postage N150

8 Paid for duplicating paper N300

12 Bought envelops N250

16 Paid Mr. Kalu N500

25 Bought office pins N100

26 Bought stamps N100

30 Paid taxi fare N200

Chillington’s Petty Cash Book

DR CR

Amount Received Date Particulars Voucher Number Total Amount Analysis of Payments

Stationery Postage Transport Office Account

2,000 Jan 1

2 Bus fare 1 200 200

4 Postage 2 150 150

8 Paper 3 300 300

12 Envelopes 4 250 250 500

16 Mr. Kalu 5 500

25 Office Pins 6 100 100

26 Stamps 7 100 100

30 Taxi fare 18 200 200

31 Balance c/d 1,800

200

300 300 400 100 500

2,000

2,000

200 Feb 1 Balance c/d

The above table is a petty cash book.

IMPREST SYSTEM

This is a method used in controlling the amount of money to the petty cashier. A fixed amount called Imprest is given to the cashier weekly or monthly to pay for small expenses.

At the end of the period, the petty cashier gives account of what she spends and the balance remaining. The amount spent will be reimbursed. This process of giving a petty cashier some amount of money for petty items at the beginning of every month is called “Imprest system”.

The sum of money giving to a petty cashier is called “Cash float”. Also, the document used in raising petty cash is known as a “Petty Cash Voucher”

Petty Cash

This is a small amount of discretionary funds in the form of cash used for expenditures where it is not sensible to make any disbursement by cheque, because of the inconvenience and costs of writing, signing and then cashing the cheque.

EVALUATION

Objectives:

1. _____________ is not found on the debit side of a petty cash book. A. Date given B. Voucher Number C. Total Amount

2. Which of the following expenditures can be paid from petty cash? A. Rent B. Equipment C. Stationery

3. The book where all small expenditure are recorded is called a __________ A. Ledger B. Petty cash book C. Journal

Theory:

A. What is a Petty Cash Book?

B. List three items contained in a petty cash book

C. State three advantages of a Petty Cash Book

PREVIEW

1. Book keeping – Ledger Entries: ledger, meaning of ledger,

2. Items on a ledger – date, particulars, folio, Discount – amount,

3. How to record cash received/payments: discount received, discount allowed and contra entries

Full Content

Meaning of Ledger:

A ledger is the principal book of account where all accounting entries are recorded. It usually has numbered pages to enable it to be easily identified from other book of account. Each page is called a Folio, and the number in it is called Folio number. A Ledge is drawn as follows:

ITEMS ON A LEDGER/LEDGER ENTRIES

DEBIT (DR) CREDIT(CR)

DATE PARTICULARS FOLIO AMOUNT DATE PARTICULARS FOLIO AMOUNT

N K N K

Entries on the left side are DEBIT ENTRIES Entries on the right side are CREDIT ENTRIES

1. Date: this column is for recording the day, mount and year the transaction took place

2. Particulars: this column explains the type of transaction that took place, e. g sales, purchase and name of individual that is involved in the transaction

3. Folio: this column is used in entering the page number of the journal from which from which the posting to the ledger account is made

4. Discount: this column is for entering the discount received for proper reconciliation when cost is being calculated.

5. Amount: this column is used to record the actual monetary value in Naira and Kobo.

HOW TO RECORD CASH RECEIVED/PAYMENT

EXAMPLE: If Mr. Hassan made the following transactions, they will be posted in a three – column cash book:

March 1. Cash at hand 200

Cash in bank 2,000

1. Withdrawal of office cash 300

2 Customer R. Adelai settle his account of

N200 by cash and was allowed 5% discount

4 Paid wages by cheque 700

5 Receive cheque from R.Winla 1,160

5 Allowed him discount 0

5 Purchase of goods less 5% discount

(Discount received) by cash 400

6 Paid T. Chike by cheque 280

Discount received 20

6 Bought packaging materials for cash 20

7 Cash sales 3,000

7 Paid into bank 2,800

What was the balance brought down on 7th Mar,2005?

Mr. Hassan’s Three Column Cash Book for March 2005

Date Particulars Folio Disct. Allwd Cash Bank Date Particulars Folio Disct. Received Cash Bank

Mar 1

Mar 2

Mar 2

Mar 5

Mar 7

Mar 7

Oct. 1 Balance

Bank

R. Adelai

R. Winla

Sales

Cash

Balance b/d

cc

b/d

10

40

200

300

190

3000

2,000

1160

2,800 Mar 2

Mar 4

Mar 5

Mar 6

Mar 6

Mar 7

Mar 7 Office Cash

Wages

Purchases

T. Chike

Packing mat.

Bank

Balance

cc

20

20

380

20

2,800

490 300

700

280

4,680

50 3,690 5,960 40 4,500 8,000

490 4,680

From Mr. Hassan’s Cash Book, the following ledgers can be drawn:

Dr Office A/c Cr

Date Particulars Amount N Date Particulars Amount

Mar 2

Bank 300

Dr Bank A/c Cr

Date Particulars Amount N Date Particulars Amount

Mar 2 Bank

300

Dr R. Adelai A/c Cr

Date Particulars Amount N Date Particulars Amount

Apr 1 Balance c/d 200 Mar 2

Mar 2 Cash

Discount 190

10

Dr Wages A/c Cr

Date Particulars Amount N Date Particulars Amount

Mar 4

Bank 700

Dr R. Winla A/c Cr

Date Particulars Amount N Date Particulars Amount

Apr 1

Balance b/d 1,200 Mar 5

Mar 5 Bank

Discount 1,160

40

1,200

Dr Purchase A/c Cr

Date Particulars Amount N Date Particulars Amount

Mar 5

Mar 5

Cash

Discount 380

20 Apr 1 Balance c/d 400

400

Dr T. Chike A/c Cr

Date Particulars Amount N Date Particulars Amount

Mar 6

Mar 6

Bank

Discount 280

20 Apr 1 Balance c/d 300

300

Dr Packing Materials A/c Cr

Date Particulars Amount N Date Particulars Amount N

Mar 6

Cash 20

Dr Sales A/c Cr

Date Particulars Amount N Date Particulars Amount N

Mar 7 Cash 800

Dr Discount Received A/c Cr

Date Particulars Amount N Date Particulars Amount

Mar 5

Mar 6

Purchases

T. Chike 20

20 Apr 1 Balance c/d 40

40

Dr Discount Allowed A/c Cr

Date Particulars Amount N Date Particulars Amount

Mar 2

Mar 5 R. Adelai

R. Winla 10

40

Dr Cash Account Cr

Date Particulars Amount N Date Particulars Amount N

Mar 7 Cash 2,800

Further Explanations

1. Discount Received: This is the cash rebate given to the seller by his suppliers of goods. It is recorded on the credit side of the cash book and on the debit side of the ledger

2. Discount Allowed: This is the cash rebate given to the buyers of goods by the seller. It is usually recorded on the debit side of the cash book and on the credit side of the ledger.

3. Contra Entries: the word contra is a Latin word meaning opposite. In some cases in business, there may be excess cash in hand which needs to be paid into the bank for official use. These are known as contra entries because both sides of the cash book will have entries concerning each transaction. Contra entries are denoted by “c” or “cc” in the folio columns and on the ledger. A bank that is credited in the cash book will be debited, while cash debited on the cash book will be credited.

EVALUATION

Objectives:

1. ___________ is not a column in the ledger. (a) Date B. Folio C. Cash

2. _________ is a column for entering page numbers. A. Particulars B. Folio C. Discount

3. The debit side of the ledger is at the _______ A. left-hand side B. right-hand side C. centre side

4. The column used for recording the actual monetary value is called ______ A. folio B. discount C. Amount

Theory:

1. Define Ledger

2. List four items posted on the debit side of a ledger

Record the following in the appropriate ledger account of Tochukwu Nwufo:

2. a. Folio 28

Jan 1 he owed the business N2000

Jan 10 he was goods worth N3,500

Jan 15 he paid N4,000 cash to the business

Jan 22, receive a debt note of N550

Jan 25 receive a credit note of N150

WEEK 5

BOOK KEEPING: Petty Cash Book

Preview

1. Book keeping – petty cash book: meaning of petty cash book,

2. preparation of petty cash book,

3. Imprest system – petty cash, refinement and reimbursement.

Full Content

PETTY CASH BOOK

This is used to record small expenses such as postage stamps, envelops, transport fares, newspapers, stationery and other small items needed in the office. The word ‘petty’ means small or unimportant. We cannot pay for them with cheques because they are too small. It is also a book of original entry and also a ledger account for petty cash. The cost of each of the small items is recorded in the petty cash book instead of the ledger. The total expenses are transferred to the ledger as a petty cash account.

Columns In a Petty Cash Book

DEBIT SIDE

1. Amount

2. Date

3. Particulars of expenses

4. Voucher number

5. Total amount

CREDIT SIDE

On the credit side we have the analysis of expenses of a ledger account. This has different columns for different expenses e. g stationery, postage, transport, etc.

Recording of Receipts and Payments in Petty Cash Book

1. The credit entry is made in the cash book

2. The debt entry is made in the petty cash book

3. The entries on the credit side of the petty cash book are first made in the total column and then, extended into the relevant expenses column,

4. The expenses columns have various headings for different expenses,

5. The last column of the petty cash book is known as a ledger account.

Preparation of a Petty Cash Book

Example

Record the following in the relevant columns of the petty cash book of Chillington, a sole proprietor.

Jan 1. Petty cashier received an Imprest amount of N2000

2 Paid for bus fare N200

4 Paid for postage N150

8 Paid for duplicating paper N300

12 Bought envelops N250

16 Paid Mr. Kalu N500

25 Bought office pins N100

26 Bought stamps N100

30 Paid taxi fare N200

Chillington’s Petty Cash Book

DR CR

Amount Received Date Particulars Voucher Number Total Amount Analysis of Payments

Stationery Postage Transport Office Account

2,000 Jan 1

2 Bus fare 1 200 200

4 Postage 2 150 150

8 Paper 3 300 300

12 Envelopes 4 250 250 500

16 Mr. Kalu 5 500

25 Office Pins 6 100 100

26 Stamps 7 100 100

30 Taxi fare 18 200 200

31 Balance c/d 1,800

200

300 300 400 100 500

2,000

2,000

200 Feb 1 Balance c/d

The above table is a petty cash book.

IMPREST SYSTEM

This is a method used in controlling the amount of money to the petty cashier. A fixed amount called Imprest is given to the cashier weekly or monthly to pay for small expenses.

At the end of the period, the petty cashier gives account of what she spends and the balance remaining. The amount spent will be reimbursed. This process of giving a petty cashier some amount of money for petty items at the beginning of every month is called “Imprest system”.

The sum of money giving to a petty cashier is called “Cash float”. Also, the document used in raising petty cash is known as a “Petty Cash Voucher”

Petty Cash

This is a small amount of discretionary funds in the form of cash used for expenditures where it is not sensible to make any disbursement by cheque, because of the inconvenience and costs of writing, signing and then cashing the cheque.

EVALUATION

Objectives:

1. _____________ is not found on the debit side of a petty cash book. A. Date given B. Voucher Number C. Total Amount

2. Which of the following expenditures can be paid from petty cash? A. Rent B. Equipment C. Stationery

3. The book where all small expenditure are recorded is called a __________ A. Ledger B. Petty cash book C. Journal

Theory:

A. What is a Petty Cash Book?

B. List three items contained in a petty cash book

C. State three advantages of a Petty Cash Book

WEEK 4

CASH BOOK

PREVIEW

(a) Meaning of Cash Book

(b) Types of Cash Book: Single Column cash book, Double Column Cash Book.

(c) Items on a column cash book: Cash column, Bank Column and discount column

(d) Preparation of Cash Book

Meaning of Cash Book

A Cash book is a book of account for recording cash receipts and cash payments. A Cash Book is one of the most important books of account. It is used only for recording cash transaction. A cash book, apart from the ledger is also a book of original entry.

Rules for Making Entries in the Cash Book

When making entries in the cash book, the following rules should be followed:

1. Enter all cash received on the debit side of the cash book.

2. Enter all cash paid out on the credit side of the cash book.

3. Enter the name of the receiver and the payer in the particular’s column

Types of Cash Book

There are three types of Cash Book

a. Single Column Cash Book

b. Double Column Cash Book

c. Three-Column Cash Book

We shall discuss each of these in detail:

Single Column Cash Book

The single Column Cash Book is drawn as follows:

Dr Cr

Date Particulars Folio Amount Date Particulars Folio Amount

It can be seen that Cash Book is divided into two equal parts, namely: the Debit side and the Credit side.

An Example is given below:

Mr. Akubo commenced business as a petty trade in Lagos, on 1st of March, 2011 with N8000 in cash. During the month, the following transactions took place: N

1. Mar. Bought office furniture 400.00

3 Mar. Bought assorted goods for sale 2000.00

5 Mar. Bought postage stamps 10.00

7 Mar. Sold goods for cash 80.00

8 Mar. Paid for cleaning materials 10.00

10 Mar. Received cash from Danladi Abubakar 50.00

14 Mar. Paid Adewale Adewunmi 90.00

16 Mar. Bought Stationery for cash 5.00

18 Mar. Bought sundry articles for resale 500.00

20 Mar. Received cash from Mallam Lamido 100.00

22. Mar. Cash Sales 50.00

24. Mar. Paid Jemima Johnson Cash 100.00

28 Mar. Paid wages to assistant 100.00

30 Mar. Paid rent 50.00

You are required to post the above entries to the cash book.

SOLUTION

The Cash Book of Mr. Akubo will be as follows

Date Particulars Folio Amount Date Particulars Folio Amount

1 Mar

7 Mar

10 Mar

20 Mar

22 Mar

1 Apr Capital

Sales

Danladi Abubakar

Lamido

Sales

Balance L.1

L.5

L.7

L.10

L.5

b/d 8,000.00

80.00

50.00

100.00

50.00 1 Mar

3 Mar

3 Mar

14 Mar

16 Mar

18 Mar

24 Mar

28 Mar

30 Mar

31 Mar Furniture

Purchases

Postage Stamps

Cleaning Materials

Adewale Adewunmi

Stationery

Purchases

Jemima Johnson

Wages

Rent

Balance L.2

L.3

L.4

L6

L.8

L.9

L.3

L.11

L.12

L.13

c/d 400.00

2,000.00

10.00

10.00

90.00

5.00

500.00

100.00

100.00

50.00

5,015.00

8,280.00 8,280.00

5,015.00

Two-Column Cash Book

A two-column cash book is used for recording a combination of bank and cash transactions. It has one column for each of cash and bank transactions on both debit and credit sides. It is drawn as follows:

Dr Cr

Date Particulars Folio Cash Bank Date Particulars Folio Cash Bank

Rules for Making Entries in the Two-Column Cash Book

Sometimes money is taken from the bank to a cash box in an office or shop. At other times, cash is taken from the office or shop and paid into the bank. Such transfer is called Contra Entry. They must be recorded in book accounts: cash and Bank accounts. Contra Entry is denoted with ‘cc’. The word ‘Contra’ is Latin word which means ‘opposite’

For example, when money is transferred from the cash box in an office, the bank receives the money, and is therefore debited, the cash account which gives the money, must also be credited.

Example:

Enter the following transactions in a double –column cash book of Olorunfemi Enterprises from the following particulars:

May 1 Cash in office 260.00

May 1 Cash at Bank 1,800.00

May 3 Received bank cheque from R. Yomi 160.00

May 5 Cash Sales to date 500.00

May 6 Paid cash into bank 650.00

May9 Paid R. Yomi by cheque 140.00

May 12 Paid rent by cheque 100.00

May 14 Bought Stationery by cash 100.00

May 17 Withdraw cash from bank to office 400.00

May 18 Purchase goods for cash 160.00

May 29 Cash sales to date 600.00

May 30 Paid cash to the bank 150.00

May 31 Paid wages in cash 100.00

May 31 Bank desired charges 50.00

Olorunfemi Enterprises Cash Book for May

Dr Cr

Date Particulars Folio Cash Bank Date Particulars Folio Cash Bank

May 1

May 3

May 5

May 6

May 17

May 29

May 30

June 1 Balance

R. Yomi

Sales

Cash

Bank

Sales

Cash

Balance b/d

cc

cc

cc

b/d 260

500

400

600 1,800

160

650

150 May 6

May 9

May 12

May 14

May 17

May 18

May 30

May 31

May 31 Bank

R. Yomi

Rent

Stationery

Cash

Purchases

Bank

Wages

Bank Charges

Balance cc

cc

cc

c/d 650

100

160

150

100

600

140

100

400

50

2,070

1,760 2,760 1,760 2,760

600 2,070

The Three Column Cash Book

The three column cash book is the same with the two-column cash book but with an additional column for discounts on both sides of the account.

Dr Cr

Date Particulars Folio Discount Allowed Cash Bank Date Particulars Folio Discount Received Cash Bank

Rules for Making Entries in the Two-Column Cash Book

The Discount column in the debit side records discount allowed to customers by the organization while the credit side records discount received by the organization.

Example: Record the following transactions in a three column cash book

N

Sept 1 Cash in Hand 500.00

Sept. 2 Received cheque from Joe 8,000.00

Sept. 2 Allowed Joe Discount 200.00

Sept. 4 Drew Cheque for Peter 2,200.00

Sept. 4 Received discount from Peter 400.00

Sept. 16 Bought goods in cash 250.00

Sept. 20 Received cash from Evans 4,000.00

Sept. 25 Paid Cash to Udoh 500.00

Sept. 30 Drew cheque for trade expenses 1,200.00

Workings

Dr Cr

Date Particulars Folio Disct. Allwd Cash Bank Date Particulars Folio Discount Received Cash Bank

Sept 1

Sept 2

Sept 20

Oct. 1 Balance

Joe

Evans

Balance b/d

b/d

200 500

4,000

8,000 Sept 4

Sept 16

Sept 25

Sept 30 Peter

Purchases

Udoh

Expenses

Balance

c/d 400

250

500

3,750 2,200

1,200

4,600

4,500 8,000 4,500 8,000

3,750 4,600

Evaluation:

Objectives:

1. A single-column cash book contains the following except: A. Date B. Bank C. Folio

2. Which of the following form of cash book does not exist? A. Single-Column cash book b. Double Column cash book c. Four-column Cash book.

3. The inducement given to a customer to encourage prompt payment is called______ A. cash discount B. Cash encouragement C. Trade discount

Theory:

Madam Adule commenced business on

June 1 With Cash 10,000.00

June 1 Paid to Bank 5,000.00

June 2 Bought goods with cash 3,000.00

June 10 Received cash from Ebuka 1,700.00

June 12 Bought Office Furniture 200.00

June 15 Paid Mr Aloba Aloe 340.00

Discount allowed by Aloba 20.00

June 20 Paid Tete Dimka 200.00

You are required to prepare Madam Adule’s Cash Book as at 30th June.

PREVIEW

(a) Meaning of Cash Book

(b) Types of Cash Book: Single Column cash book, Double Column Cash Book.

(c) Items on a column cash book: Cash column, Bank Column and discount column

(d) Preparation of Cash Book

Meaning of Cash Book

A Cash book is a book of account for recording cash receipts and cash payments. A Cash Book is one of the most important books of account. It is used only for recording cash transaction. A cash book, apart from the ledger is also a book of original entry.

Rules for Making Entries in the Cash Book

When making entries in the cash book, the following rules should be followed:

1. Enter all cash received on the debit side of the cash book.

2. Enter all cash paid out on the credit side of the cash book.

3. Enter the name of the receiver and the payer in the particular’s column

Types of Cash Book

There are three types of Cash Book

a. Single Column Cash Book

b. Double Column Cash Book

c. Three-Column Cash Book

We shall discuss each of these in detail:

Single Column Cash Book

The single Column Cash Book is drawn as follows:

Dr Cr

Date Particulars Folio Amount Date Particulars Folio Amount

It can be seen that Cash Book is divided into two equal parts, namely: the Debit side and the Credit side.

An Example is given below:

Mr. Akubo commenced business as a petty trade in Lagos, on 1st of March, 2011 with N8000 in cash. During the month, the following transactions took place: N

1. Mar. Bought office furniture 400.00

3 Mar. Bought assorted goods for sale 2000.00

5 Mar. Bought postage stamps 10.00

7 Mar. Sold goods for cash 80.00

8 Mar. Paid for cleaning materials 10.00

10 Mar. Received cash from Danladi Abubakar 50.00

14 Mar. Paid Adewale Adewunmi 90.00

16 Mar. Bought Stationery for cash 5.00

18 Mar. Bought sundry articles for resale 500.00

20 Mar. Received cash from Mallam Lamido 100.00

22. Mar. Cash Sales 50.00

24. Mar. Paid Jemima Johnson Cash 100.00

28 Mar. Paid wages to assistant 100.00

30 Mar. Paid rent 50.00

You are required to post the above entries to the cash book.

SOLUTION

The Cash Book of Mr. Akubo will be as follows

Date Particulars Folio Amount Date Particulars Folio Amount

1 Mar

7 Mar

10 Mar

20 Mar

22 Mar

1 Apr Capital

Sales

Danladi Abubakar

Lamido

Sales

Balance L.1

L.5

L.7

L.10

L.5

b/d 8,000.00

80.00

50.00

100.00

50.00 1 Mar

3 Mar

3 Mar

14 Mar

16 Mar

18 Mar

24 Mar

28 Mar

30 Mar

31 Mar Furniture

Purchases

Postage Stamps

Cleaning Materials

Adewale Adewunmi

Stationery

Purchases

Jemima Johnson

Wages

Rent

Balance L.2

L.3

L.4

L6

L.8

L.9

L.3

L.11

L.12

L.13

c/d 400.00

2,000.00

10.00

10.00

90.00

5.00

500.00

100.00

100.00

50.00

5,015.00

8,280.00 8,280.00

5,015.00

Two-Column Cash Book

A two-column cash book is used for recording a combination of bank and cash transactions. It has one column for each of cash and bank transactions on both debit and credit sides. It is drawn as follows:

Dr Cr

Date Particulars Folio Cash Bank Date Particulars Folio Cash Bank

Rules for Making Entries in the Two-Column Cash Book

Sometimes money is taken from the bank to a cash box in an office or shop. At other times, cash is taken from the office or shop and paid into the bank. Such transfer is called Contra Entry. They must be recorded in book accounts: cash and Bank accounts. Contra Entry is denoted with ‘cc’. The word ‘Contra’ is Latin word which means ‘opposite’

For example, when money is transferred from the cash box in an office, the bank receives the money, and is therefore debited, the cash account which gives the money, must also be credited.

Example:

Enter the following transactions in a double –column cash book of Olorunfemi Enterprises from the following particulars:

May 1 Cash in office 260.00

May 1 Cash at Bank 1,800.00

May 3 Received bank cheque from R. Yomi 160.00

May 5 Cash Sales to date 500.00

May 6 Paid cash into bank 650.00

May9 Paid R. Yomi by cheque 140.00

May 12 Paid rent by cheque 100.00

May 14 Bought Stationery by cash 100.00

May 17 Withdraw cash from bank to office 400.00

May 18 Purchase goods for cash 160.00

May 29 Cash sales to date 600.00

May 30 Paid cash to the bank 150.00

May 31 Paid wages in cash 100.00

May 31 Bank desired charges 50.00

Olorunfemi Enterprises Cash Book for May

Dr Cr

Date Particulars Folio Cash Bank Date Particulars Folio Cash Bank

May 1

May 3

May 5

May 6

May 17

May 29

May 30

June 1 Balance

R. Yomi

Sales

Cash

Bank

Sales

Cash

Balance b/d

cc

cc

cc

b/d 260

500

400

600 1,800

160

650

150 May 6

May 9

May 12

May 14

May 17

May 18

May 30

May 31

May 31 Bank

R. Yomi

Rent

Stationery

Cash

Purchases

Bank

Wages

Bank Charges

Balance cc

cc

cc

c/d 650

100

160

150

100

600

140

100

400

50

2,070

1,760 2,760 1,760 2,760

600 2,070

The Three Column Cash Book

The three column cash book is the same with the two-column cash book but with an additional column for discounts on both sides of the account.

Dr Cr

Date Particulars Folio Discount Allowed Cash Bank Date Particulars Folio Discount Received Cash Bank

Rules for Making Entries in the Two-Column Cash Book

The Discount column in the debit side records discount allowed to customers by the organization while the credit side records discount received by the organization.

Example: Record the following transactions in a three column cash book

N

Sept 1 Cash in Hand 500.00

Sept. 2 Received cheque from Joe 8,000.00

Sept. 2 Allowed Joe Discount 200.00

Sept. 4 Drew Cheque for Peter 2,200.00

Sept. 4 Received discount from Peter 400.00

Sept. 16 Bought goods in cash 250.00

Sept. 20 Received cash from Evans 4,000.00

Sept. 25 Paid Cash to Udoh 500.00

Sept. 30 Drew cheque for trade expenses 1,200.00

Workings

Dr Cr

Date Particulars Folio Disct. Allwd Cash Bank Date Particulars Folio Discount Received Cash Bank

Sept 1

Sept 2

Sept 20

Oct. 1 Balance

Joe

Evans

Balance b/d

b/d

200 500

4,000

8,000 Sept 4

Sept 16

Sept 25

Sept 30 Peter

Purchases

Udoh

Expenses

Balance

c/d 400

250

500

3,750 2,200

1,200

4,600

4,500 8,000 4,500 8,000

3,750 4,600

Evaluation:

Objectives:

1. A single-column cash book contains the following except: A. Date B. Bank C. Folio

2. Which of the following form of cash book does not exist? A. Single-Column cash book b. Double Column cash book c. Four-column Cash book.

3. The inducement given to a customer to encourage prompt payment is called______ A. cash discount B. Cash encouragement C. Trade discount

Theory:

Madam Adule commenced business on

June 1 With Cash 10,000.00

June 1 Paid to Bank 5,000.00

June 2 Bought goods with cash 3,000.00

June 10 Received cash from Ebuka 1,700.00

June 12 Bought Office Furniture 200.00

June 15 Paid Mr Aloba Aloe 340.00

Discount allowed by Aloba 20.00

June 20 Paid Tete Dimka 200.00

You are required to prepare Madam Adule’s Cash Book as at 30th June.

WEEK 5

PITMAN SHORTHAND (VOWEL PLACEMENT) FIRST, SECOND AND THIRD

PREVIEW

I. Vowels Placement(first, second and third),

II. Types of vowels(e,e,o, and u),

III. word drills

Full Content

In J.S. One, we learnt that Shorthand is an art of representing spoken words by written signs. In other words, words are written as they sound and not how they are spelt

Vowels, in Shorthand, are written in different positions of an outline. The position of any vowel determines the sound of the outline. It enables one to know whether an outline is a first place outline or a third place outline. You will remember that a vowel can be placed at the beginning, middle and at the end of a stroke, as illustrated thus:

……………… First Place (at the Beginning of the stroke)

………… Second Place (at the middle of the stroke)

……. Third Place (At the end of the stroke)

First place Vowel

When a first place vowel is the first vowel in a word, the outline is written in the first place position, that is the first downstroke or upstroke is written above the line. Then the vowels are written at the beginning of the stroke.

Example: Long vowel /ah/ is represented by a heave dot.

.

Pa = Ma = .

Second Place Vowel

When a second place vowel is the first vowel in a word, the outline is written in the second position, that is the first down stroke or upstroke rests on the line. Then the vowels are written at the middle of the outline or stroke.

Example:

Pay = . Bay = .

Third Place Vowel

When a third place vowel is the first vowel in a word, the outline is written in third place position, that is the first downstroke or upstroke is written through the line.

When a third place vowel comes between two strokes, it is put in the third place before the second stroke.

Example:

Tea = Eat =

. .

Types of Vowels

a. Vowel e

This long vowel /e/ is represented by a heavy dot. It is placed at the middle of a stroke. It is a second place vowel. Example as in

Day = . Date = .

b. Vowel e

The Short light sound vowel /e/ (as in fed) is represented by a dot, which is placed at the middle of the stroke. It is a second place vowel. Example as in

Beg = . Peg = .

c. Vowel /o/

This is a long sounded vowel and it is represented by a heavy dash. It is a second place vowel, therefore, it is written at the middle of the stroke.

Example as in:

Toe = - Bow = -

d. Vowel /u/

This is a short sounded vowel and is represented by a light dash. It is a second place vowel. It is therefore placed in the middle of the stroke.

Example as in:

Up = - tug = -

EVALUATION

Objectives:

1. Third place vowels are placed at the……………………. A. Beginning B. Bottom C. Side

2. Vowels are placed on the ……………….. A. Signs B. Sounds C. Strokes

3. Vowel ‘e’ is represented with a ---------- (a) light dot (b) light dash (c) heavy dot

4. In a word like cup, the ‘u’ is represented with a ------- (a) light dot (b) light dash (c) heavy dash

Theory:

1. Transcribe the following: pay, palm, calm, take, date, bay, Edet

2. What happen when a vowel comes before the stroke, where is it written?

3. Where is the second place vowel written?

WEEK 8

Pitman Shorthand (Third group of consonants and vowels)

PREVIEW

1. Consonants and Vowels – Third group of consonants ( k, g m, n, ng, I , w, y),

2. First place Vowels(ah, oo, aw)

3. Third place Vowels ( e, I, oo, oo)

Full Content

Third group of consonants

The third group of Shorthand Consonants is K, G, M, N, Ng, L, W and Y. They are represented by horizontal strokes and curves. One thing is common to these consonants, they are all written forward

Note:

When a vowel comes before a horizontal stroke, it is written above the stroke; when a vowel comes after a horizontal stroke, it is written below the stroke.

Examples

. . . . .

Came gay egg may cake

Word Drills

Way low tale bell ache lake

Delay yellow goal wedge who will name

------------------------------------------------------------------------------------------------------------

Egg may aim lay

-------------------------------------------------------------------------------------------------------------

Game name coal male

-------------------------------------------------------------------------------------------------------------

Way low make came

-------------------------------------------------------------------------------------------------------------

Wed led tale tail

-------------------------------------------------------------------------------------------------------------

Jail bell memo envelops

-------------------------------------------------------------------------------------------------------------

Bello Monday cake

First Place Vowels

The first place vowels are written in the first place, i.e. at the beginning of a stroke. When a first place vowel is the first vowel in a word, the outline is written in the first place position, that is the first downstroke or upstroke is written above the line.

The vowels are:

a. Vowel /a/

Long vowel /a/ is represented by a heavy dot as we have in:

. .

. .

Pa Ma Palm Calm

b. Vowel a

Short/a/ is represented by a light dot as we have in:

. . . . . .

Ada Aba bank map

c. Vowel aw

Long /aw/ is represented by a heavy dash (-) as we have in

- - -

-

Jaw talk Paw law

d. Vowel o

Short /o/ is represented by a light dash (-) as we have in:

- - - - .

Top dog mop Ota

Third Place Vowels

The third place vowels are four in number. Remember that third place outlines or strokes are written through the line. The vowels are:

a. Vowel /e/

This is a long vowel sound. It is represented by a heavy dot (.) written at the end of a stroke as in:

. . . .

Eat each keep teach

b. Vowel /i/

This is a short vowel. It is represented by a light dot.

Example:

. . . .

Bit pick big lip

c. Vowel /oo/ (as in food)

This is a long vowel. It is represented by a heavy dash.

-

-

-

Shoe tool Cool

d. Vowel /oo/

This is a third place vowel. It is also represented by a light dash.

Example

-

Took look

EVALUATION

Objectives:

1. The third group of consonants are ……………… strokes a. Horizontal and light b. curved and heavy c. horizontal and curved.

2. In using a second place vowel, the strokes must be written _________

a. Above the line b. on the line c. through the line

3. Thick and thin strokes are used to represent ……………………. A. consonants b. vowels c. Phrases

Theory:

1. Write these words in shorthand: lake, goal, came, pit, tale, lick, kill, Bell

2. Shock, church, lunch, gang, ship

WEEK 9

Pitman Shorthand (Consonants R & H)

PREVIEW

1. Consonants and Vowels – The fourth last group of consonants ( R & H),

2. Forems or R and H -Upward, downward.

3. Diphthongs and triphone -meaning

4. Shorthand outlines and signs

Full Content

Consonants /r/ and /h/ are the fourth group of Shorthand consonants because they have two different ways of representing them.

There is the upward /r/ and /h/, and also downward /r/ and /h/.

Upward R .

This is represented by a thin straight upstroke.

It is used for the following purposes

a. When /r/ begins a word, as in: Red - . Raid = .

b. When /r/ is in the middle of an outline, as in:

Purpose = - -

c. At the end of an outline when /r/ is followed by a sounded vowel as in

Borrow = - -

Downward R

Downward /r/ is a thin curve down stroke. It is used:

a. when a vowel comes before /r/ at the beginning of a word, as in

air, her, erase, earth

b. When /r/ ends a word, as in:

Care, dare, error

c. When /r/ comes before /m/, as in:

Rome, term, firm

Downward H

Downward H is usually represented by a downward stroke.

It is used when /g/ is the only consonant or if it is followed by /k/ or /g/, as in:

High, hake, hug

Upward H

This is usually represented by an upward stroke. It is used when joining /h/ to other consonants, as in:

Happy, hope, head, hero, etc.

Diphthong

This is described as two vowels being pronounced as one syllable. There are four types of this shorthand: /i/, /o/, /ow/ and /u/

Diphthong /i/ and /oi/ are first place vowel placements.

The sign for /i/ is __________

Example: Pie ________ Buy __________

Die _________ tie __________

The sign for /oi/ is ______

Example: Boy ________ Toy __________

The Diphthong /ow/ and /u/ are third place vowel placements.

The sign for /ow/ is ______

Example: Cow _________ Out _________

Loud __________ row

The sign for /u/ is ________

Example: duty ________ cure _________

The Triphone

A small tick added to the diphthong sign shows that another vowel immediately follows the diphthong. This combination is called Triphone. Therefore, a triphone is a combination of three vowels as in:

Buyer ________ Royal _________ Liar ___________

Via _________ Loyal_________ Power _________

Evaluation:

1. Write the following in Shorthand: Red, Raid, Purpose, burrow, care, dare, door, error, Rome, Room

2. Transcribe the following into Shorthand: Happy, Hero, hurry, home, health

PREVIEW

I. Vowels Placement(first, second and third),

II. Types of vowels(e,e,o, and u),

III. word drills

Full Content

In J.S. One, we learnt that Shorthand is an art of representing spoken words by written signs. In other words, words are written as they sound and not how they are spelt

Vowels, in Shorthand, are written in different positions of an outline. The position of any vowel determines the sound of the outline. It enables one to know whether an outline is a first place outline or a third place outline. You will remember that a vowel can be placed at the beginning, middle and at the end of a stroke, as illustrated thus:

……………… First Place (at the Beginning of the stroke)

………… Second Place (at the middle of the stroke)

……. Third Place (At the end of the stroke)

First place Vowel

When a first place vowel is the first vowel in a word, the outline is written in the first place position, that is the first downstroke or upstroke is written above the line. Then the vowels are written at the beginning of the stroke.

Example: Long vowel /ah/ is represented by a heave dot.

.

Pa = Ma = .

Second Place Vowel

When a second place vowel is the first vowel in a word, the outline is written in the second position, that is the first down stroke or upstroke rests on the line. Then the vowels are written at the middle of the outline or stroke.

Example:

Pay = . Bay = .

Third Place Vowel

When a third place vowel is the first vowel in a word, the outline is written in third place position, that is the first downstroke or upstroke is written through the line.

When a third place vowel comes between two strokes, it is put in the third place before the second stroke.

Example:

Tea = Eat =

. .

Types of Vowels

a. Vowel e

This long vowel /e/ is represented by a heavy dot. It is placed at the middle of a stroke. It is a second place vowel. Example as in

Day = . Date = .

b. Vowel e

The Short light sound vowel /e/ (as in fed) is represented by a dot, which is placed at the middle of the stroke. It is a second place vowel. Example as in

Beg = . Peg = .

c. Vowel /o/

This is a long sounded vowel and it is represented by a heavy dash. It is a second place vowel, therefore, it is written at the middle of the stroke.